Curious Beginner's Guide to Crypto

Explain like I'm five crypto concepts

Level up your product and creator skills in just 5 min a week. Join 50,000+ readers:

Dear subscribers,

In this post, my goal is to “explain like I’m five” the following:

Web 3

Blockchain

Fungible and non-fungible tokens

Bitcoin and Ethereum

NFTs

DAOs

It’s often easier to learn from a curious beginner than an expert who speaks in jargon. This post is for curious beginners - let’s go down the rabbit hole together.

Web 3

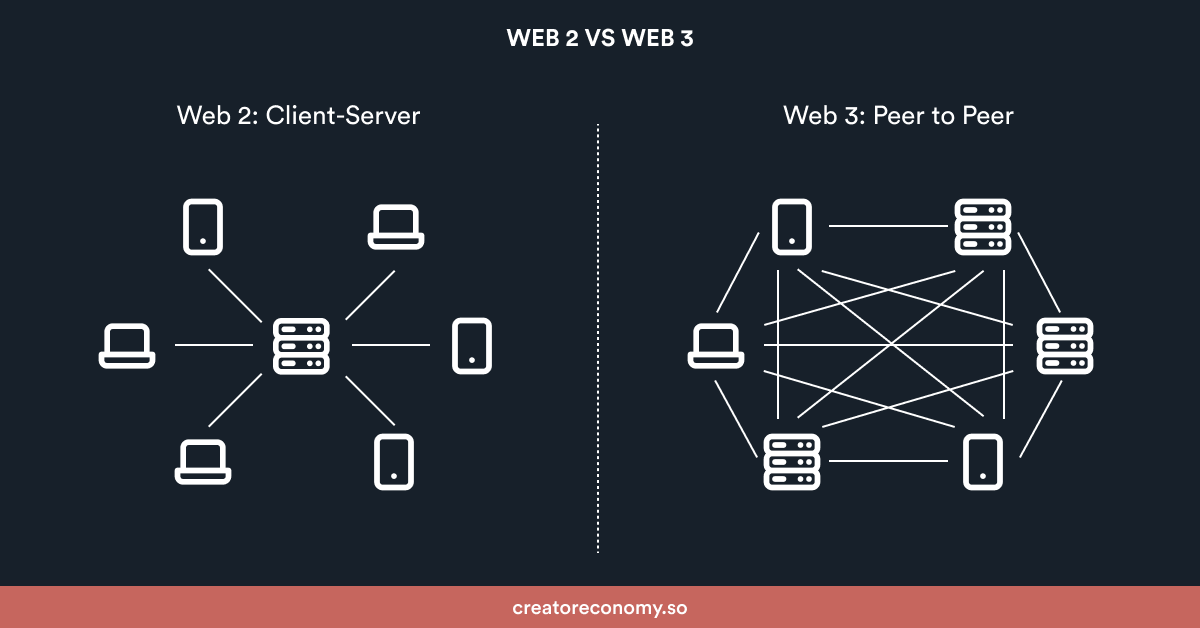

The best way to explain web 3 is to compare it to web 2.

Web 2 is the internet today, dominated by tech giants. It’s built off client-server architecture where users are the client and companies control the servers.

Web 3 is the internet that’s been pioneered by crypto. It’s built off peer-to-peer networks of computers that talk to each other without middlemen using blockchain tech.

Learn more:

Blockchain

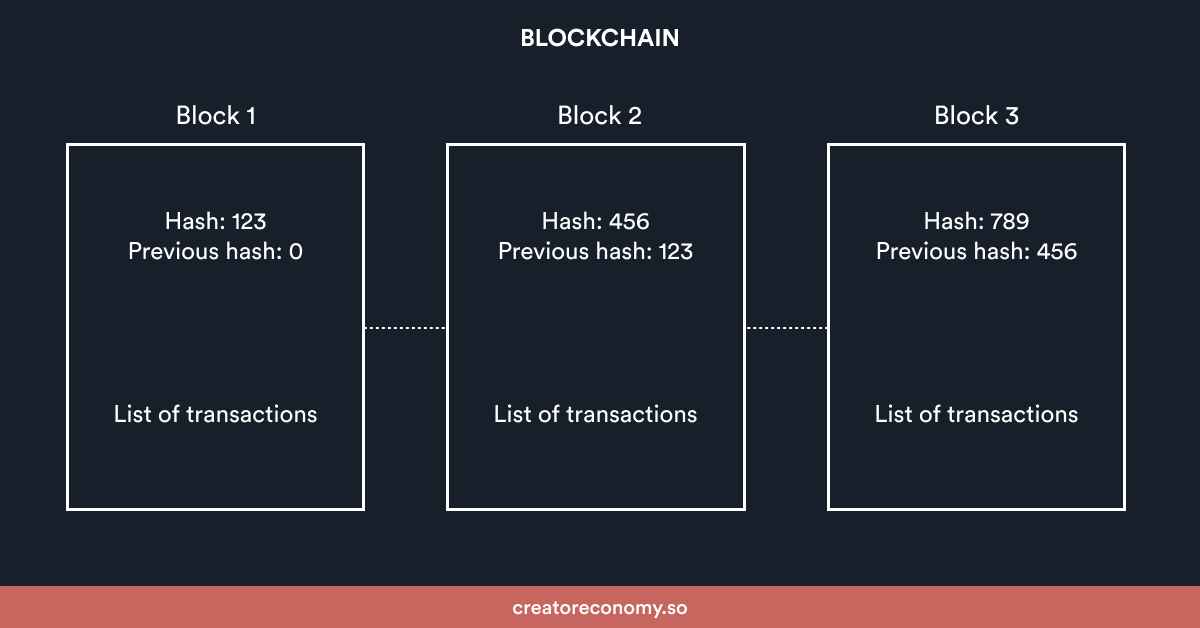

A blockchain is a linked list of transactions stored on a network of computers.

Blockchains are:

Decentralized: Transactions are stored on a network of computers (nodes).

Immutable: Transactions cannot be changed once committed to the block.

Open: Transactions can be viewed by anyone.

Each block has:

A list of transactions

A hash (a long string of random characters) for the block

The previous block’s hash (this is how the blocks are linked)

Let's take a look at how a transaction works on the blockchain.

Learn more:

Blockchain: Wallets and keys

Suppose Bob wants to send Mary 1 bitcoin.

First, both Bob and Mary need crypto wallets. These wallets are either software (e.g., Coinbase, Metamask, Rainbow) or hardware (e.g., Ledger).

Crypto wallets don’t actually store funds. Instead, they store two keys:

A public key links to an address that lets you send and receive transactions. Think of it as your email address.

A private key proves that you own the tokens associated with your public address. Think of it as your email password. Since a private key is hard to remember (it’s a very long string of random numbers), wallets also give you a 12-24 word seed phrase.

Bob can send Mary 1 bitcoin in three steps:

Bob tells his wallet: "I want to send 1 bitcoin from my public address to Mary's public address." Bob's wallet produces a digital signature for this transaction based on his private key. This signature proves that Bob actually owns 1 bitcoin.

Bob's wallet sends the transaction to nodes on the blockchain network. These nodes then verify the transaction using Bob’s signature and public key.

A node groups Bob’s transaction with other transactions into a block. It then works with other nodes to add the block to the blockchain.

Mary will see 1 bitcoin in her wallet only after all three steps are complete.

The most important takeaway when it comes to wallets and keys is:

You can share your public key with others to send and receive transactions.

You must never share your private key or seed phrase. If someone has access to these artifacts, they’ll be able to make transactions on your behalf.

We mentioned above that a block can be added to the blockchain only if other nodes agree. Let’s explore how nodes reach consensus next.

Learn more:

Blockchain: Consensus mechanisms

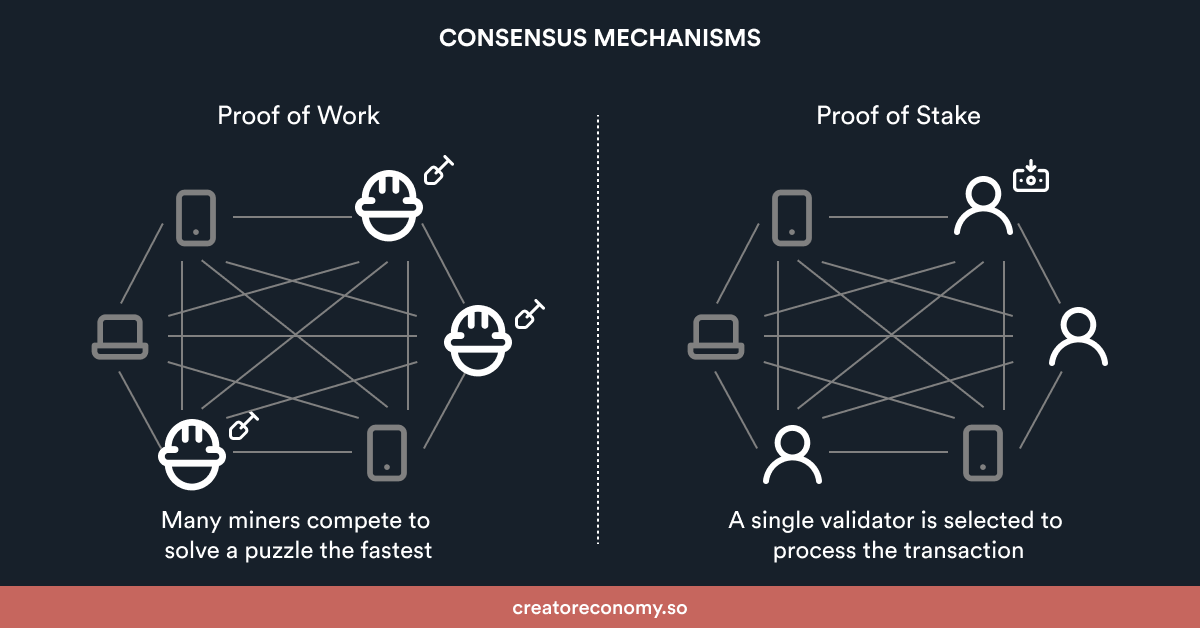

To process transactions without trusting middlemen, nodes need to be able to reach consensus themselves. They do this through two popular methods:

Proof of work

Nodes called miners compete to solve a math problem using brute force (e.g., rolling a dice thousands of times to get the right number).

The first miner that solves the problem gets to create a block.

Other nodes check if the block is valid. If it is, the miner is rewarded cryptocurrency. If it’s not, the miner wasted their time and energy.

All nodes add the new block to their copy of the blockchain.

Proof of work uses energy because miners compete to solve math problems by building powerful machines that run 24/7.

Proof of stake

Nodes called validators stake some cryptocurrency. A stake is like saying: “I’ll commit this amount of cryptocurrency to win the right to do this transaction.”

Validators with more stake are more likely (but not guaranteed) to be selected to process the transaction and create a block.

Other validators check if the block is valid. If it is, all participating validators earn a transaction fee. If it’s not, the validator that created the block might lose its stake.

All nodes add the new block to their copy of the blockchain.

Proof of stake is still in its infancy but uses less energy than proof of work. Bitcoin uses proof of work, and Ethereum is currently transitioning from proof of work to proof of stake.

Now that we know how blockchain works, let’s talk about tokens.

Learn more:

Fungible vs. Non-fungible tokens

A token is a record of ownership of an asset.

Tokens can be fungible or non-fungible:

Fungible tokens are interchangeable (e.g., Bitcoin, Ether).

Non-fungible tokens (NFTs) are unique (e.g., a piece of art).

As an example, let’s look at a game like Fortnite or Roblox:

Fungible tokens are the game’s virtual currency (e.g., VBucks, Robux).

Non-fungible tokens (NFTs) are the game’s character skins, emotes, and more.

Two of the most popular fungible tokens (aka cryptocurrencies) are bitcoin and ether (the token for Ethereum).

Learn more:

Bitcoin

Bitcoin was created in 2009 by Satoshi Nakamoto (a pseudonym) to be a “peer-to-peer electronic cash system.” (Bitcoin whitepaper)

Today, many people also use bitcoin as a store of value (think digital gold).

Bitcoin uses blockchain and therefore is decentralized, immutable, and open. It’s also:

Hard capped: There will only ever be 21M bitcoin.

Single-purpose: Many holders just want it to be a digital token that stores value.

Not everyone agrees with the last statement. Projects like Stacks and Lightning are working to expand Bitcoin’s use cases.

But most people don’t want Bitcoin to change. After all, if Bitcoin becomes the best way to store value and lets anyone send money around the world, that’s already a huge accomplishment.

Yet Bitcoin is not where a lot of the development in crypto is. That’s happening in...

Learn more:

Ethereum

Ethereum was created in 2013 by Vitalik Buterin to let anyone “write smart contracts and decentralized applications (dapps).” (Ethereum whitepaper)

To understand what that even means, let’s define the following:

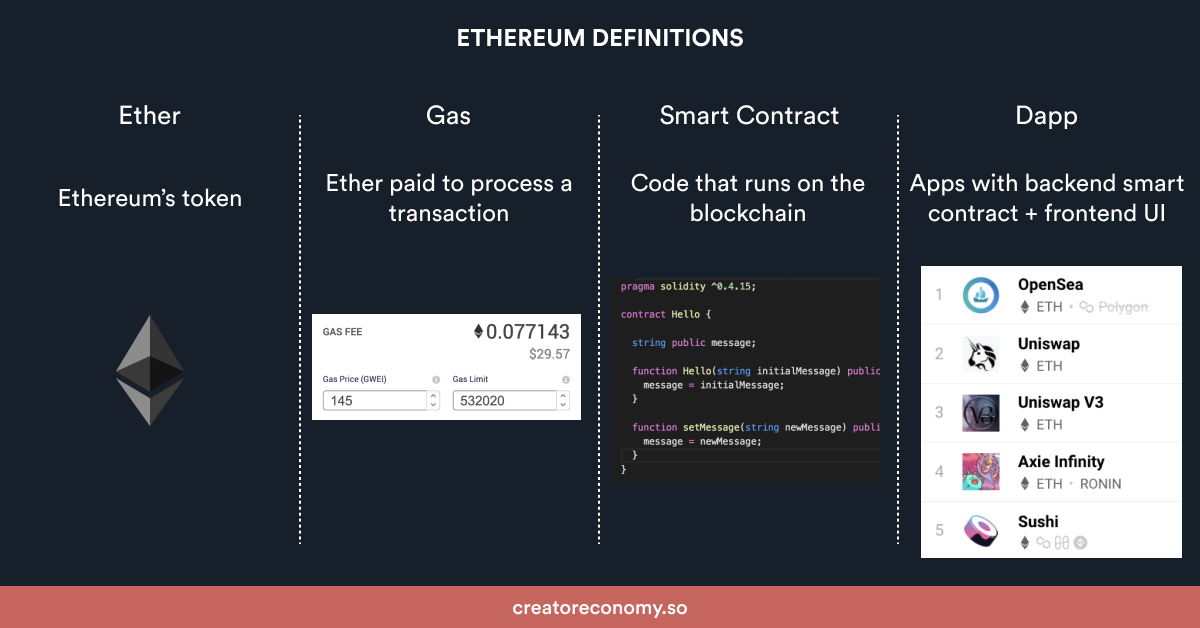

Ether is Ethereum’s digital token. Ether is a store of value like Bitcoin, but its main purpose is to reward nodes on the ethereum blockchain for processing transactions.

Gas is the amount of Ether that’s paid to a node to process a transaction.

Smart contracts are code that runs on the Ethereum blockchain. This code is:

Decentralized: Stored across all nodes in the network.

Immutable: Can’t be changed once committed to the blockchain.

Open: Anyone can view the code and use it (like an open API).

Decentralized apps (dapp) combine a backend smart contract with frontend UI.

Dapps are where the action is in crypto and the majority are built on Ethereum. Examples include:

OpenSea for buying and selling digital assets.

Uniswap for swapping digital tokens.

Decentraland for owning land in a 3D digital world.

All of these dapps cost gas to run. That’s why Ethereum is upgrading to eth 2.0 (which includes shifting from proof of work to stake) to scale the network, reduce energy consumption, and lower gas fees.

Learn more:

Other cryptocurrencies

Bitcoin and Ethereum together have 60% market share, but other cryptocurrencies like Solana are also on the rise. We won’t cover them here, but it’s important to note:

There’s usually a trade-off between scalability, security, and decentralization.

For example, as of this writing:

Solana’s average transaction cost is $0.00025 with 1,000 validator nodes.

Ethereum’s average transaction cost is $3.8 with 10,000+ validator nodes.

The more nodes there are, the less likely it is for a network to become compromised. This post isn’t about which cryptocurrency is better - just remember that this trade-off exists.

Learn more:

Non-fungible tokens (NFTs)

An NFT is a record of ownership of a unique asset.

This record lives on the blockchain and is:

Decentralized: Stored on a network of computers.

Immutable: Cannot be changed once committed.

Open: Anyone can see the transaction history.

Types of NFTs

To understand why people are buying NFTs, let’s look at a few popular types:

1/1s are single assets. The artist Beeple sold a 1/1 NFT for $69M at Christie’s.

Collectibles are sets of assets. Popular collectible categories include:

Sports: NBA Top Shots feature video clips of top NBA moments. Dapper Labs, which built Top Shots, is now valued at $7.6M.

Profile picture (PFPs): CryptoPunks (lowest price $292K) and Bored Ape Yacht Club (lowest price $115K) are two popular PFP projects. They each feature 10K profile pic NFTs. BAYC has also built an amazing community and roadmap.

Generative art: ArtBlocks (lowest price for curated is $4.6K) uses an algorithm to produce art that can be minted as NFTs.

“Lego blocks”: Loot features simple text lists of adventure gear. The idea is that NFT owners will build experiences on top of loot (e.g., images of items to even full games).

Learn more:

A Step by Step Guide to NFTs for Creators (by yours truly)

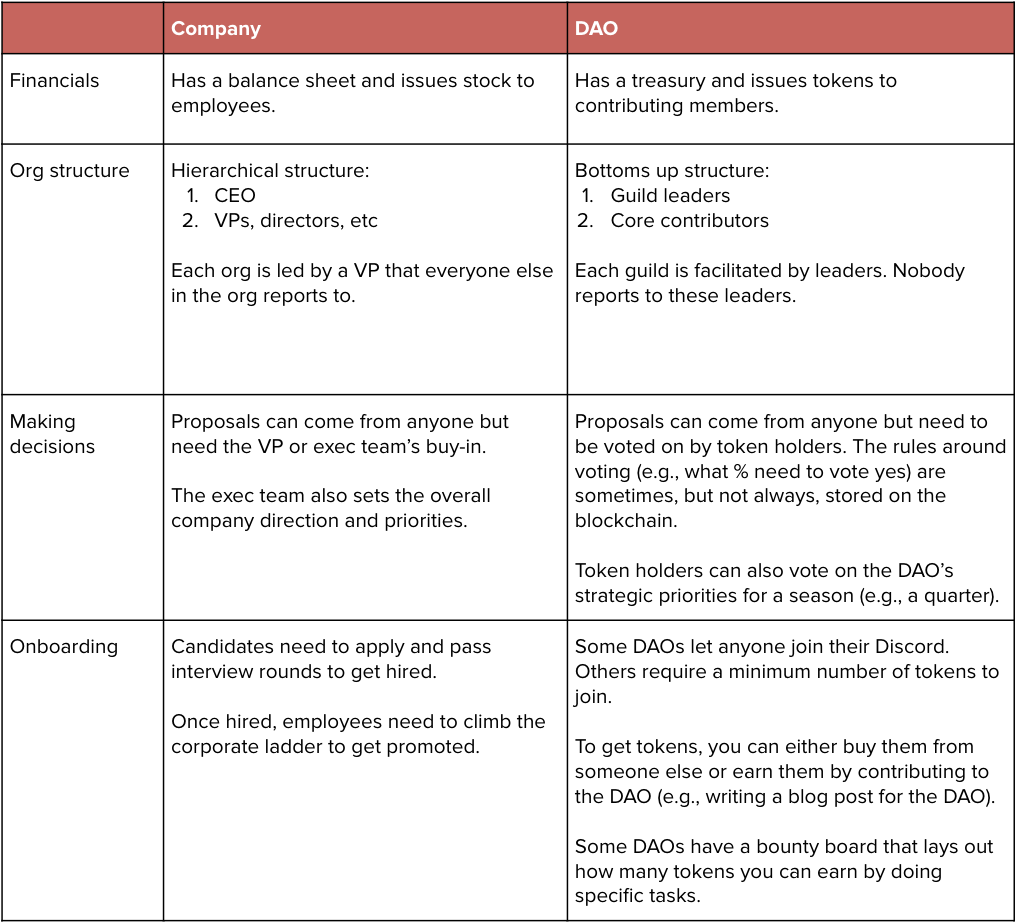

DAOs

A DAO is a community with a treasury owned by its contributing members.

The simplest way to describe how a DAO works is to compare it to a company:

Here are a few examples of DAOs:

Friends with Benefits: FWB is a private social club that builds products and offers IRL private events. To join, you need to hold 75 $FWB tokens (~$8K).

Flamingo DAO: Flamingo invests in NFTs and lets the community co-own them. In January 2021, Flamingo bought a rare Cryptopunk for 605 eth (~$761K).

Uniswap DAO: Uniswap is a protocol that lets people swap tokens. In 2020, it issued its own UNI token to let community members vote on how to evolve the protocol.

Here’s the bottom line for DAOs:

Proposals get approved by other token holders vs. a hierarchical management chain.

People can earn tokens by putting in the work to help the DAO.

DAOs are unproven - many have perished.

Learn more:

If you made it this far, then congrats - you’re a curious beginner in crypto.

Crypto is the wild west - explore it carefully.

Subscribe below to level up your product and creator skills in just 5 min a week:

If you enjoyed this post, consider taking a moment to:

Refer a friend to unlock my 180+ page PM book and paid subscriptions for free.

Sponsor this newsletter to reach 50,000+ tech professionals and creators.

this post was so educational and concise - ty!

For Proof of Stake - "Other validators check if the block is valid. If it is, all participating validators earn a transaction fee. If it’s not, the validator that created the block might lose its stake."

Aren't validators in this scenario just another type of middle man? Banks are the middle man today and take a transaction fee, and validators are doing the same to process the transaction. I'm sure that's an inaccurate analogy, but i'm not sure how.. How do you think about validators and transaction fees in relation to processes we have today?